Nvidia(NASDAQ: NVDA) has been among the best long-term investments of all time. Since 1999, shares have elevated in worth by greater than 285,000%, pushing the corporate’s market capitalization into the trillions of {dollars}. The reason for Nvidia’s hovering valuation has been the rise of synthetic intelligence (AI).

However Nvidia is not the one firm uncovered to the huge tailwind that’s AI spending. Long run, there’s one other chipmaker that might find yourself giving Nvidia a run for its cash. And in contrast to Nvidia’s inventory, this comparatively small competitor is not priced for perfection, that means affected person buyers may gain advantage from each fast long-term progress charges and a reduced valuation.

Almost everyone seems to be nicely conscious of the leap in AI innovation that has occurred lately. The ChatGPT web site receives a number of billion guests each month, and the corporate’s COO lately revealed that it has greater than 400 million lively month-to-month customers, up from round 300 million just some months in the past. Amazingly, this progress occurred at the same time as ChatGPT confronted heavy competitors from different AI fashions like DeepSeek, which itself has gained lots of of thousands and thousands of recent customers.

However all of this progress remains to be on the end-user aspect. Proper now, there’s additionally an enormous uptake in AI adoption amongst companies, though adoption charges general for companies within the U.S. stay underneath 10%. That gives an enormous runway for long-term progress. And similar to within the web’s early days, the last word energy and pervasiveness of this paradigm-shifting expertise will probably be arduous to overestimate.

Take into account the most recent analysis from world consultancy McKinsey & Co. Generative AI alone, the agency believes, might produce $2.6 trillion to $4.4 trillion in financial affect from enterprise adoption alone. By 2040, it believes income from AI software program and providers will attain $1.5 to $4.6 trillion, up from simply $85 billion in 2022. Put merely, the tempo and scale of the AI revolution will probably be even higher than most predict.

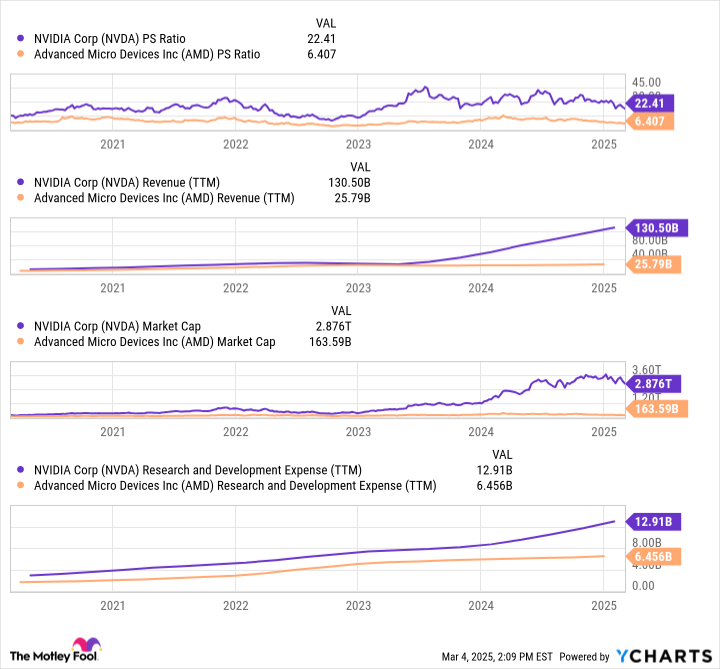

That is nice information for Nvidia. Its graphics processing models (GPUs) — vital elements that make it potential for AI providers and purposes to exist — are thought of the most effective within the enterprise, granting the corporate a market share someplace between 70% and 95% for AI GPUs. However as earlier chip wars have demonstrated, market shares range over lengthy stretches of time, and Nvidia’s dominant place could not final eternally. However even when it does, there ought to be loads of market to promote into.

All that offers the corporate beneath a shiny future regardless of a dramatically smaller market cap versus Nvidia right now.

It will likely be a really troublesome feat, but when I needed to choose one firm to match Nvidia’s dimension inside a decade from now it will be Superior Micro Units(NASDAQ: AMD). The corporate is at a steep drawback proper now when it comes to technological capabilities and vendor lock-in. However it’s making all the fitting investments to compete over the long run.

Proper now, AMD’s market worth is a small fraction of Nvidia’s. And its valuation, no less than when it comes to multiples just like the price-to-sales ratio, is significantly smaller as nicely. However the firm has managed to proceed upping its analysis and improvement funds regardless of these headwinds. That funds is round 25% of its income base proper now. Nvidia’s, whereas bigger on an absolute foundation, totals simply 10% of its gross sales base.

AMD’s continued investments are permitting it to launch next-gen graphics playing cards for gaming like its Radeon RX 9000 collection playing cards. However its additionally permitting it to slowly meet up with Nvidia for AI GPUs. The launch of its MI325X chips will enable it to compete extra straight with Nvidia’s Blackwell chips, and administration lately famous that it is going to be accelerating its product schedule to launch new chips on an annual schedule to raised compete and capitalize on the growth in demand for AI chips.

Will AMD overtake Nvidia over the subsequent seven years? Nvidia’s personal explosive rise has proven that it is potential. However it is going to be an extended, troublesome highway. Happily, the corporate continues to reinvest in new merchandise, efforts that ought to be rewarded long run given regularly rising end-market demand. At a fraction of Nvidia’s valuation, AMD is a good speculative guess for affected person progress buyers.

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for buyers to purchase now… and Nvidia wasn’t one among them. The ten shares that made the reduce might produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our advice, you’d have $677,631!*

Now, it’s price notingInventory Advisor’s whole common return is822% — a market-crushing outperformance in comparison with166%for the S&P 500. Don’t miss out on the most recent high 10 listing, accessible once you be a part ofInventory Advisor.

Ryan Vanzo has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Units and Nvidia. The Motley Idiot has a disclosure coverage.