Amazon Eyes $320 as AWS Development Fuels Bullish Outlook

Fast Learn

-

Amazon (AMZN) reported Q1 EPS of $2.78, crushing the $1.73 estimate, with income at $181.5B (up 16.61%), AWS reaccelerating to twenty-eight% development (its quickest tempo in 15 quarters), and customized chips reaching a $20B run charge with triple-digit development.

-

24/7 Wall St. has a 12-month worth goal of $320.08 (20.76% upside) with a purchase score at 90% confidence.

-

AWS capability commitments from OpenAI (2 GW), Anthropic (5 GW), and over 1 million NVIDIA GPUs in 2026 present multi-year demand visibility, however capital depth stays a threat with Q1 capex up 77% to $44.2B and full-year 2026 capex guided close to $200B.

-

The analyst who known as NVIDIA in 2010 simply named his high 10 shares and Amazon wasn’t considered one of them. Get them right here FREE.

Amazon delivered a clear earnings report, and our mannequin leans into the energy. Amazon (NASDAQ:AMZN) trades at $265.06 after rising 27.27% over the previous month, however our proprietary work suggests the rally has room.

Our 24/7 Wall St. worth goal is $320.08 over the following 12 months, implying 20.76% upside. The advice is purchase with 90% confidence.

The analyst who known as NVIDIA in 2010 simply named his high 10 shares and Amazon wasn’t considered one of them. Get them right here FREE.

24/7 Wall St. Value Goal Abstract

|

Metric |

Worth |

|---|---|

|

Present Value |

$265.06 |

|

24/7 Wall St. Value Goal |

$320.08 |

|

Upside |

20.76% |

|

Suggestion |

BUY |

|

Confidence Degree |

90% |

A Cloud Reacceleration That Modifications the Math

Amazon shares are up 14.83% yr up to now and 43.73% over the previous yr, close to the 52-week excessive of $265.91. The Q1 2026 report on April 29 was the catalyst. EPS of $2.78 beat the $1.73 estimate, income grew 16.61% to $181.519 billion, and AWS reaccelerated to twenty-eight% development, its quickest tempo in 15 quarters.

Promoting crossed $70 billion in trailing twelve-month income, customized chips topped a $20 billion run charge rising triple digits, and Shops unit development hit 15%, the very best since COVID lockdowns ended. The April 21 announcement of a further $25 billion Anthropic funding tied to a 5GW compute dedication flipped retail sentiment from bearish to bullish in roughly two weeks.

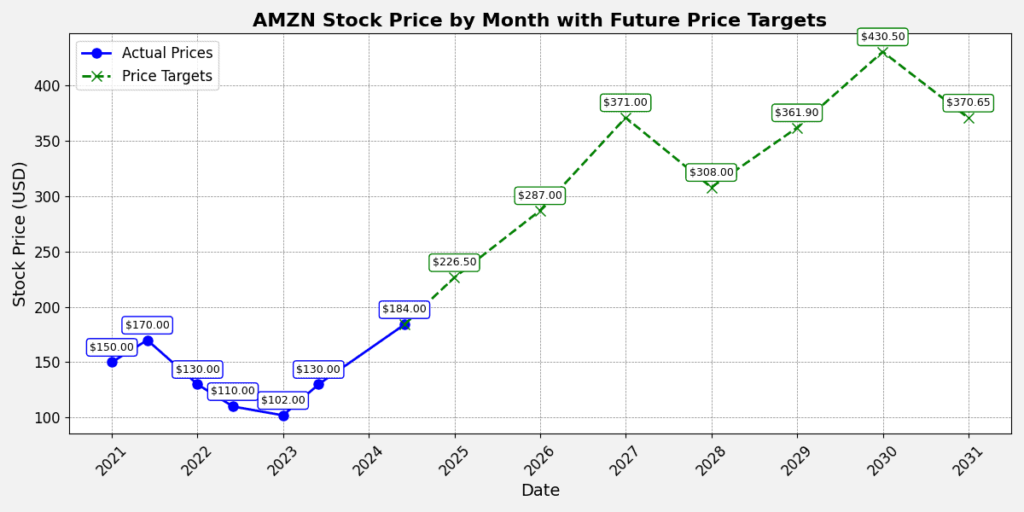

The Case for $371 and Past

Bulls have actual runway. The OpenAI dedication of two GW of Trainium capability starting 2027, Anthropic’s 5 GW dedication, and over 1 million NVIDIA GPUs deploying in 2026 lock in multi-year AWS demand visibility.

Analyst sentiment helps this: 65 purchase or sturdy purchase scores versus 4 holds and nil sells. Our bull case factors to $371.56 by Could 2027, a 40.18% complete return, achievable if AWS holds 28%-plus development and promoting sustains 24% momentum.