The Empire Strikes Again: The majors and Merlin gained (a bit) of market share on Spotify final yr.

It’s turn into a perennial commerce music trade story: The mixed world market share of the three main report corporations and Merlin on Spotify is in decline.

Properly, no extra.

In 2025, based on Spotify, this long-running development was truly reversed. By a sliver, anyway.

Earlier than we get into the numbers, some essential clarification:

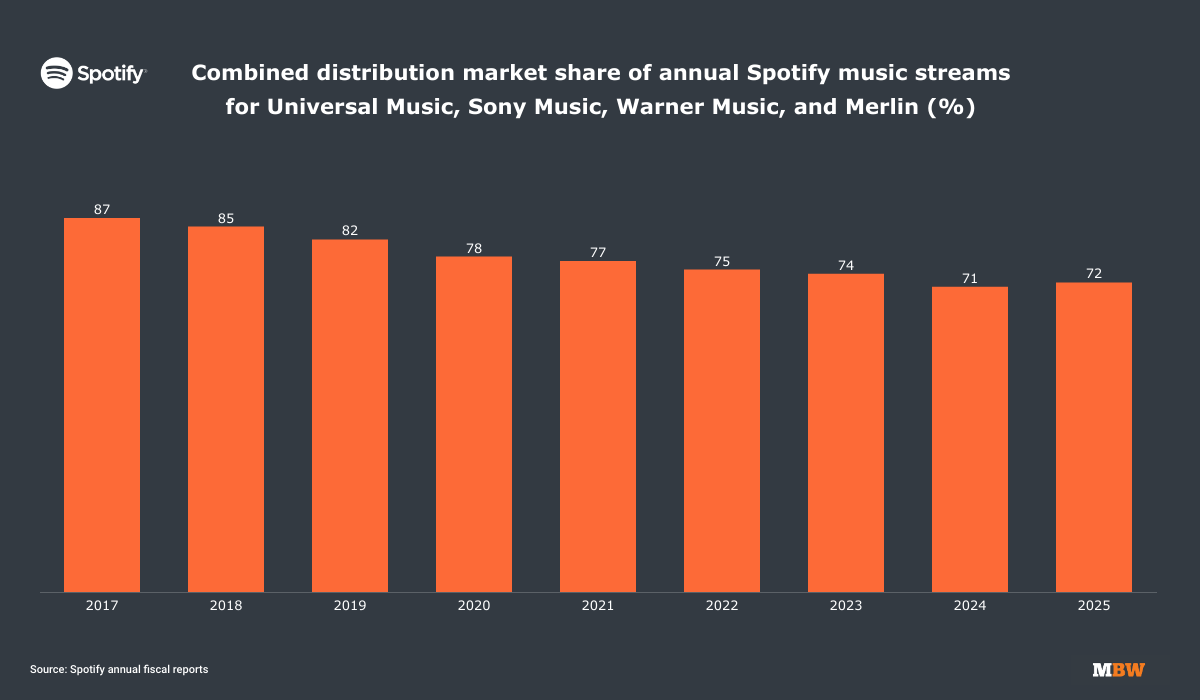

- This important market-share stat, confirmed by Spotify in its annual fiscal report, reveals the platform’s yearly ‘stream share’ for all recorded music represented by Common, Sony, Warner – together with their ‘indie’ distribution arms – plus Merlin.

- ‘Stream share’ on this context means the mixed entities’ market share of the whole world quantity of music streams on Spotify (i.e. not together with audiobooks and podcasts).

- Entities not coated by the stat embrace any label or distributor that licenses Spotify exterior of offers inked by UMG/Sony/Warner/Virgin/The Orchard/AWAL/ADA/Merlin.

- This non-major/Merlin cohort consists of DistroKid, Empire, and Imagine/TuneCore, plus BMG, which started distributing its catalog to Spotify immediately in 2023. It additionally consists of massive Merlin members who select to license Spotify immediately, relatively than by way of Merlin’s opt-in collective agreements.

- To reiterate: It is a measurement of streaming quantity market share; it’s subsequently unaffected by any adjustments to Spotify’s royalty fashions (together with the so-called ‘artist-centric’ royalty frameworks).

With that every one understood, let’s dig in.

From 2017 to 2024, the majors-plus-Merlin cohort noticed their mixed annual quantity market share of music performs on Spotify persistently decline, from 87% in 2017 all the way in which right down to 71% in 2024 – a 1,600 foundation level decline.

Throughout the identical interval (2017-2024), recorded music corporations not represented by the majors or Merlin on Spotify noticed their mixed market share develop considerably, from 13% in 2017 to 29% in 2024.

In 2025, based on Spotify’s new 20-F annual report, the majors-plus-Merlin cohort gained a degree of market share. Its repertoire accounted for 72% of all world music performs, whereas non-major or Merlin corporations accounted for 28%.

This was the primary time in Spotify’s historical past as a public firm that majors-plus-Merlin have grown their market share YoY.

Elements value contemplating on this story embrace the high-streaming purchasers represented by Merlin and/or the indie arms of the most important music corporations. Not least The Orchard, which distributed the largest album on Spotify globally final yr – Unhealthy Bunny’s DeBÍ TiRAR MáS FOToS.

In the meantime, the most important music corporations represented all ten of the greatest albums on Spotify final yr, together with the Ok-pop Demon Hunters soundtrack (by way of UMG’s Republic Information) at No.2, Hit Me Laborious And Comfortable by Billie Eilish (by way of UMG’s Interscope) at No.3, SZA’s SOS LANA version (by way of Sony’s RCA) at No.4, and Sabrina Carpenter’s Brief N Candy (by way of Island/UMG) at No.5.

The majors additionally represented all the High 10 songs on Spotify globally in 2025 – in contrast to in 2024, when No.4 (Gata Solely) was distributed by UnitedMasters.

The most important labels’ world dominance of the famous person market, nonetheless, is one thing we’ve lengthy been accustomed to.

Flip this story round, and there’s maybe a much bigger narrative at play.

One of many components within the decline of the majors’ Spotify market share over the previous decade has been the collective streaming progress pulled in by the voluminous so-called ‘middle-class’ of artists – i.e. commercially significant acts working method beneath the worldwide High 10 (and certainly, the High 100) lists of every yr.

A lot of this ‘middle-class’ artist progress has taken place exterior the partitions of UMG, Sony, and Warner. So have the ‘huge three’, notably by way of their indie arms, now begun making extra vital headway into this a part of the market?

One other potential consider 2025’s numbers is perhaps Merlin increasing its member base throughout areas worldwide.

One also needs to clearly contemplate the ability of M&A: for instance, UMG solely accomplished its 100% acquisition of indie stalwart [PIAS] in October 2024, which means the resultant market share shift from this transfer wouldn’t absolutely present up in Spotify’s annual numbers till 2025.

UMG’s greatest indie-sector acquisition transfer of current years, after all, hasn’t occurred but: its pending nine-figure acquisition of Downtown Music Holdings.

Save for a probable carve-out of royalty platform Curve, the Common/Downtown deal is anticipated to be lastly cleared by European regulators any time quickly.Music Enterprise Worldwide